1 July 2025 to 30 June 2026

Australian Taxation Office (ATO) and government revenue authority review activity continues to be shaped by increased funding, expanding data matching capabilities and a growing focus on risk based reviews.

Recent Federal Budget measures have provided significant additional funding for ATO review programs, while other government revenue authorities continue to strengthen their own review and verification activities. Together, these developments suggest review activity will remain a prominent feature of the Australian tax landscape for years to come.

Using claims data compiled by the Accountancy Insurance claims team, this article examines how Audit Shield claims activity changed between 1 July 2025 to 30 June 2026 and 1 July 2024 to 30 June 2025, identifies the most prevalent sources of professional fee exposure and explores some of the factors influencing review activity across Australia.

How claims activity has shifted year on year

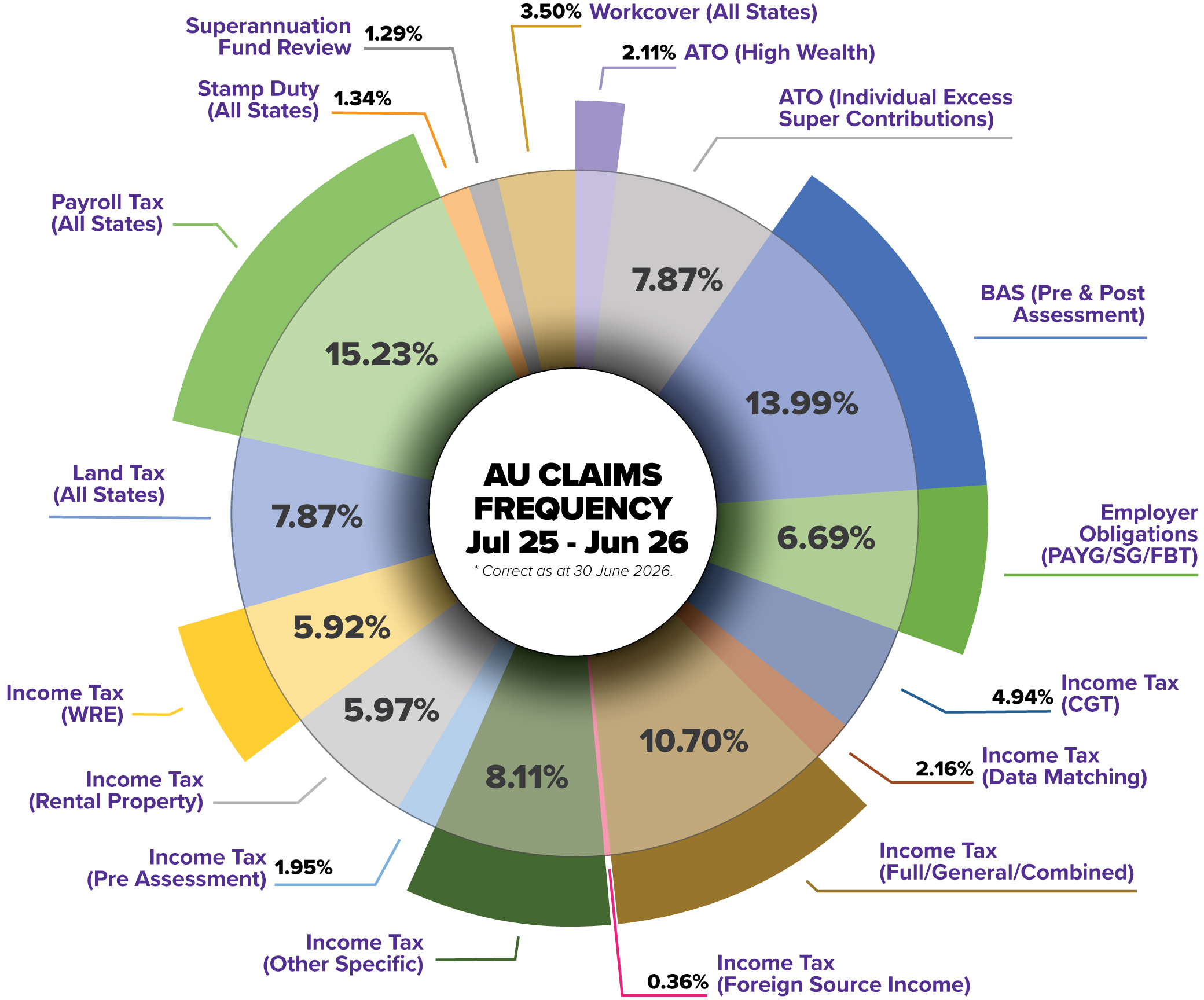

Based on claims lodged between 1 July 2025 to 30 June 2026 as of 30 June 2026, the three most frequent Audit Shield claim categories compiled by the Accountancy Insurance claims team were:

- Payroll Tax (All States) – 15.23% (up from 14.73%)

- BAS (Pre & Post Assessment) – 13.99% (up from 10.20%)

- Income Tax (Full/General/Combined) – 10.70% (down from 11.60%)

Payroll Tax remains the largest source of claims activity

Payroll Tax remained the most prevalent Audit Shield claim category, representing 15.23% of claims activity during the period 1 July 2025 to 30 June 2026, compared with 14.73% during the period 1 July 2024 to 30 June 2025.

The continued prominence of Payroll Tax claims reflects the significant level of payroll tax review activity being undertaken by government revenue authorities. The state level breakdown highlights that payroll tax review activity is occurring across multiple jurisdictions.

Victoria remained the largest contributor, accounting for 30.85% of Payroll Tax claims during the period 1 July 2025 to 30 June 2026, although this was down from 39.93% during the period 1 July 2024 to 30 June 2025. New South Wales represented 25.42% during the period 1 July 2025 to 30 June 2026, compared with 28.21% during the period 1 July 2024 to 30 June 2025. Notably, Queensland’s share increased from 10.99% during the period 1 July 2024 to 30 June 2025 to 21.69% during the period 1 July 2025 to 30 June 2026. Western Australia increased from 16.85% during the period 1 July 2024 to 30 June 2025 to 20.34% during the period 1 July 2025 to 30 June 2026. These shifts reinforce that Payroll Tax review activity is a national issue and not concentrated within a single jurisdiction.

BAS (Pre & Post assessment) reviews become more prominent

BAS claims represented 13.99% of Audit Shield claims activity during the period 1 July 2025 to 30 June 2026, compared with 10.20% during the period 1 July 2024 to 30 June 2025. This represented one of the most significant movements in the claims data.

BAS reviews continue to arise through verification processes, analytical review techniques and ongoing monitoring activities undertaken by the ATO.

Within this category, BAS (Post Assessment) reviews represented 62.50% of all BAS claims activity during the period 1 July 2025 to 30 June 2026, while BAS (Pre Assessment) reviews represented 37.50%.

General income tax reviews remain a consistent source of professional fee exposure

Income Tax (Full/General/Combined) represented 10.70% of claims activity during the period 1 July 2025 to 30 June 2026, compared with 11.60% during the period 1 July 2024 to 30 June 2025.

Although slightly lower than the previous financial year, this category remained one of the most common sources of professional fee exposure. General income tax reviews continue to be a consistent feature of the review landscape and regularly require accountant involvement in responding to government revenue authority enquiries.

Other notable financial year on year movements

Beyond the three largest claim categories, several broader trends emerged from the latest data.

Land Tax and WorkCover activity became more prominent during the period 1 July 2025 to 30 June 2026. While these categories often receive less attention than traditional ATO reviews, their increased representation highlights the important role state based government revenue authorities continue to play in the broader review activity landscape environment.

Capital Gains Tax related claims also increased their share of overall claims activity, representing 4.94% of claims activity during the period 1 July 2025 to 30 June 2026, up from 3.83% during the period 1 July 2024 to 30 June 2025.

Conversely, some established income tax review categories, including Rental Property reviews and Data Matching reviews, represented a smaller share of overall claims activity in the period 1 July 2025 to 30 June 2026 when compared to 1 July 2024 to 30 June 2025.

Taken together, the Audit Shield claims data points to a landscape that is becoming more diverse, with professional fee exposure arising across a wider range of other government revenue authority review activities than has traditionally been the case.

Audit activity outside of the accountant’s control

During the period 1 July 2025 to 30 June 2026, more than 56% of all Audit Shield claims activity related to categories where the underlying information, transactions or business practices are often managed by the client rather than the accountant.

| Category | Claims activity |

| Payroll Tax (All States) | 15.23% |

| BAS (Pre & Post Assessment) | 13.99% |

| ATO (Individual Excess Super Contributions) | 7.87% |

| Land Tax (All States) | 7.87% |

| Employer Obligations (PAYG/SG/FBT) | 6.69% |

| WorkCover (All States) | 3.50% |

| Stamp Duty (All States) | 1.34% |

| Total | 56.49% |

Payroll Tax, WorkCover, Land Tax, Stamp Duty, Employer Obligations and Excess Super Contributions are frequently influenced by employer decisions, payroll systems, employment arrangements, property holdings and other matters that sit outside the accountant’s day to day oversight. As a result, accounting firms are often called upon to assist after review activity has commenced, rather than when the underlying circumstances first arose.

For accounting firms, the implication is clear. Professional fee exposure is not limited to traditional income tax reviews or matters directly related to tax return preparation. A significant proportion of review activity arises from areas where the underlying information and business decisions are often controlled by the client rather than the accountant.

Factors driving audit activity

Several factors continue to shape the current compliance environment.

Additional ATO funding

The 2025-26 Federal Budget included approximately $999 million in additional funding for compliance initiatives, including:

- $717.8 million for the Tax Avoidance Taskforce

- $155.5 million for the Shadow Economy Compliance Program

- $75.7 million for the Personal Income Tax Compliance Program

- $50 million for the Tax Integrity Program

Expanded data matching and third party reporting

The ATO continues to expand its use of third party reporting and analytical review techniques to identify discrepancies and areas requiring further examination. Third party reporting systems and information sharing initiatives provide government revenue authorities with increasing visibility of taxpayer transactions and activities.

Professional fee exposure arising from ATO and other government revenue authority review activity continues to extend beyond traditional income tax audits. The latest Audit Shield claims data demonstrates that reviews are occurring across an increasingly broad range of categories, including Payroll Tax, BAS, Land Tax, WorkCover, Employer Obligations and Capital Gains Tax.

More than half of all Audit Shield claims activity during the period 1 July 2025 to 30 June 2026 arose from categories that are often influenced by client-controlled information and business practices. This highlights the reality that review activity can occur even where clients receive quality professional advice and maintain appropriate records.

As the ATO and other government revenue authorities continue to invest in review programs, data matching and information-sharing initiatives, accounting firms can expect review activity to remain a regular feature of the Australian tax landscape.

About Accountancy Insurance

For more than 22 years, Accountancy Insurance has supported accounting professionals across Australia, New Zealand and Canada with solutions designed specifically for the realities of modern practice.

As ATO and government revenue authority review activity continues to evolve, accounting firms are increasingly being called upon to assist clients with audits, reviews, enquiries and investigations. Accountancy Insurance helps firms manage the financial and professional risks that arise from this changing environment.

Our specialist solutions include:

Audit Shield

Audit Shield helps protect clients against the professional fees incurred when responding to eligible audit, review, enquiry and investigation activity instigated by the ATO and other government revenue authorities.

PI Shield

Professional Indemnity insurance designed for the use of AI tools, AML changes, and evolving exposures.

Cyber Shield

A cyber insurance solution designed for accounting firms, providing access to specialist support and comprehensive protection against a range of cyber related risks and incidents.

Today, thousands of accounting firms trust Accountancy Insurance to help protect their practice, support their clients and navigate an increasingly complex regulatory environment.

To learn more about Audit Shield or any of the Accountancy Insurance solutions, contact our team.

Contact Accountancy Insurance

We would love to hear from you.